Chinese New Year in 2026 welcomes the Year of the Horse, a year symbolizing perseverance, vitality and substantial momentum, which indeed was reflected in the Chinese markets’ hotel performance over the festive holiday.

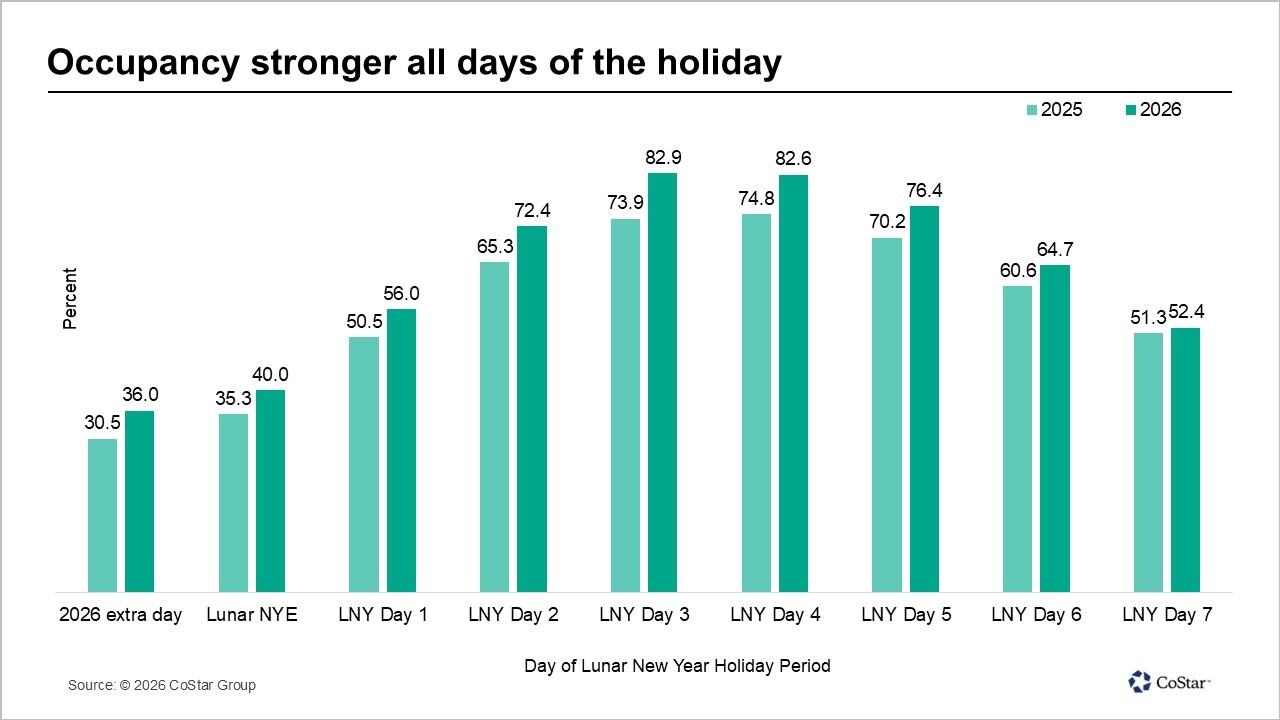

This year, the Chinese public holidays ran over nine days, including an extra day. Running from Feb. 15 to 23, this was the longest Chinese New Year holiday period in history.

Good fortune spread through all days of the week as occupancy outperformed last year on every day of the holiday period, with gains ranging from 4% to 8%. Growth was strongest at the start of the holiday before gradually easing toward the end.

The extra holiday before Lunar New Year Eve this year also helped occupancy grow above the same period in 2025.

Rate gains were also impressive and outperformed every day of the week apart from Day 6 and 7, when occupancy growth also started to weaken. Growth per day was between 2% to 7%, again gradually reducing as the holiday progressed. By Days 6 and 7, average daily rate declined relative to 2025 at -1% and -2%, respectively.

The additional day prior to Chinese New Year Eve supported the rise in pricing power and demand, as holidaymakers opted to begin the festivities earlier in the week.

Demand was the primary revenue per available room growth driver, with the metric increasing all days over the holiday period despite rate declining at the end of the week.

All classes prospered, surpassing last year’s RevPAR with double-digit growth. The only decline was luxury occupancy, which dipped 1% against the 2025 New Year. However, luxury ADR had the biggest increase, tying with midscale and economy rate growth at 20%.

The pricing power for high-end hotels surged over the New Year period. Luxury ADR grew significantly even without major increases in occupancy.

The anticipated holiday hotspots included the winter destinations of Xinjiang and Heilongjiang, the coastal favorite Sanya and Yunnan, known for its cultural richness and diversity. Three out of four markets had significant growth, all mainly rate-driven.

An alternative skiing destination to the more established Heilongjiang, Xinjiang appeals to local enthusiasts who are looking for a less costly option with fewer crowds.

On top of Heilongjiang serving as a pricier option, and also taking into consideration the travel cost for domestic tourists to get there, it didn’t help that due to slightly warmer conditions the Harbin Ice-Snow World closed on Feb. 21, three days before the end of the public holiday period.

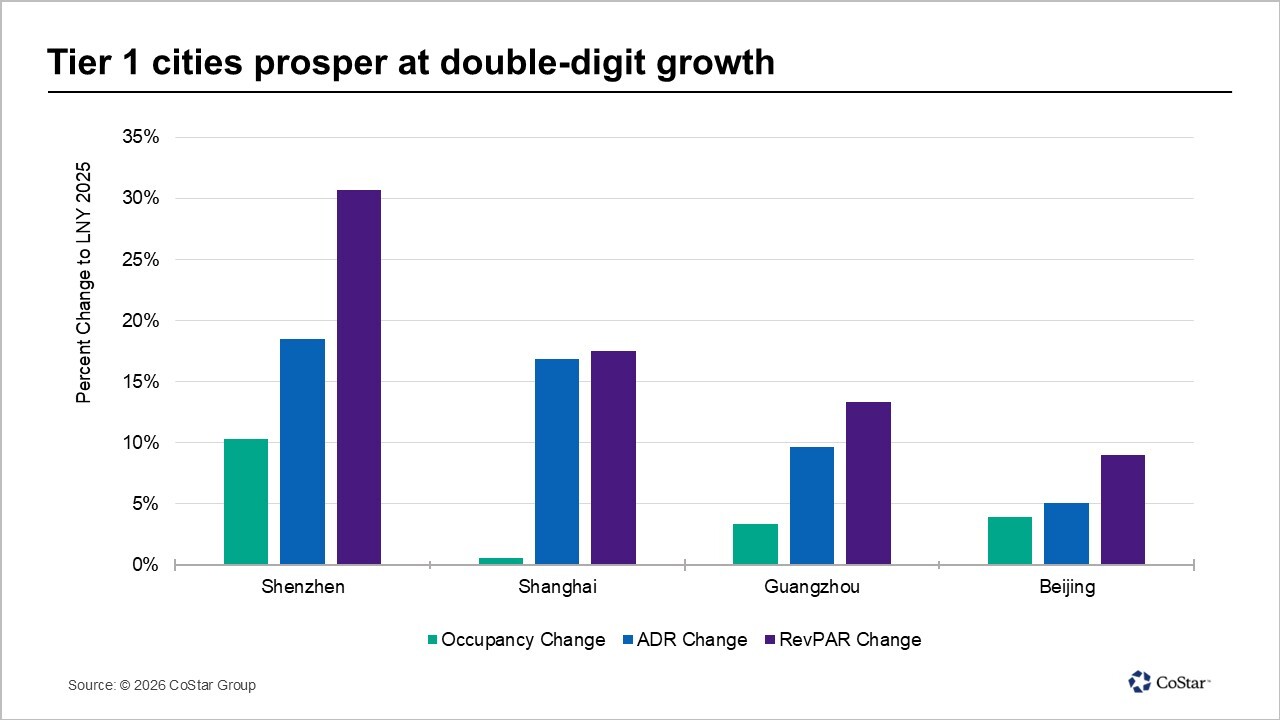

Looking at the wider picture, 18 key markets grew RevPAR between 7% to 31% year over year, indicating share of domestic demand is more evenly distributed within the country. Three out of eighteen markets — Shenzhen, Zhengzhou and Wuxi — grew during the Chinese New Year holidays in 2025 and continued to strengthen in 2026.

At the top and bottom of the key markets were tier 1 cities Shenzhen and Guangzhou. While the variance between RevPAR is wide, both markets enjoyed increasing demand and even stronger rate growth. Beijing ranks closer to Guangzhou, but Shanghai growth stands out from the four with ADR growing 18% and occupancy up 1%.

Key markets outside of Mainland China had higher growth in January, a month before the Chinese New Year holiday. Incheon and Seoul occupancy peaked twice at the beginning of the year, then normalized by mid-February. Singapore showed a similar trend, with occupancy slightly increasing over the holiday period. Meanwhile, Hong Kong SAR started the year strong but then declined during the holidays. Macau occupancy continued to gradually grow but did not see any particular impact from the new year.

Both Japan and Thailand have been closely monitored due to challenges faced with inbound travel from China. Thai markets, Bangkok and Phuket, both reported good occupancy growth during the holiday period, although the improvement started earlier in the month.

Late last year, Chinese airlines extended flight cancellations to Japan through the first quarter of 2026, with the most cancellations in February. Hotel occupancy across key markets was soft toward the beginning of the year, but by the beginning of February, occupancy started to trend up. Some of this growth overlaps with the Chinese New Year, but this period also coincides with a long weekend in Japan, as the Emperor’s birthday fell on the last day of the China public holiday period, Feb. 23.

The Year of the Horse provided the boost for Mainland China markets to start a new year with positive and energetic momentum. The longer holiday period set a foundation for rate confidence and the propensity of Chinese holidaymakers to opt for domestic destinations drives the demand needed to attain a successful new year holiday period.

Marielle Malabanan is a senior data analyst with STR, based in London.