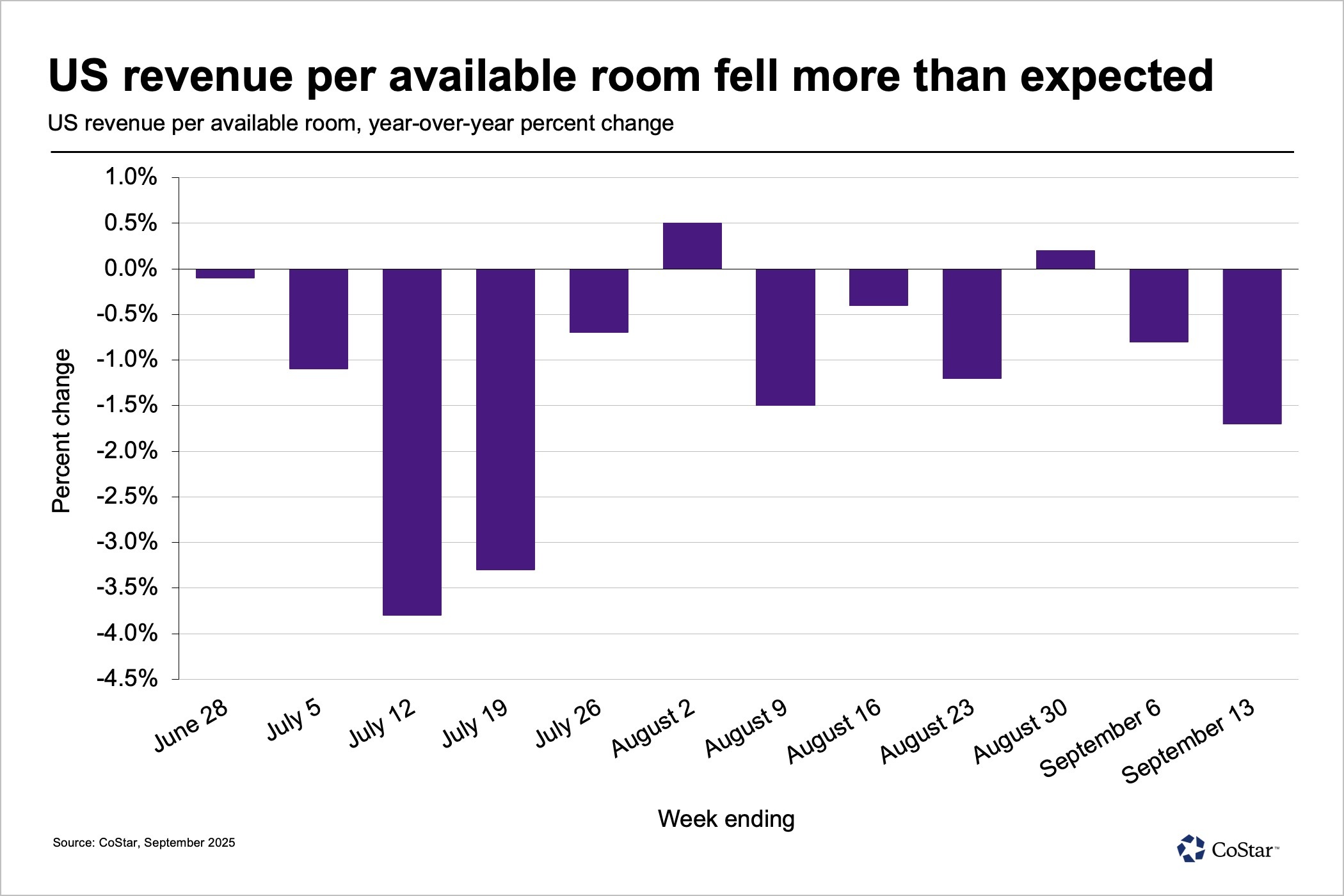

It was surprising to see U.S. hotel revenue per available room fall in the week of Sept. 7-13, as this was one of the “clean” comparable weeks in the month without any calendar shifts.

Weekly RevPAR fell by 1.7%, its largest decrease of the past eight weeks. As we have seen in most weeks this year, falling hotel occupancy drove the decline as average daily rate remained stagnant (+0.1%). Since April, U.S. hotel occupancy has dropped every week except for two. What’s even more concerning is the continuing room rate trend – ADR growth has been at or below 0.5% in 13 of the past 24 weeks.

History has pointed to good RevPAR results, but recently it has not

Based on historical hotel performance data, the week after Labor Day has varied and has been especially weak in recent years. In 2019, RevPAR in the week after Labor Day was up 0.9%. In 2022, it saw a gain of only 0.4% and fell in 2024 (-1.2%). However, in September 2014, which has the same calendar makeup as September 2025 – and with Rosh Hashanah falling in the same week as this year – RevPAR grew strongly on rising demand and ADR. Thus, U.S. hoteliers expected better performance during the week of Sept. 7-13 given the timing of the Jewish observances.

Similar to the prior week, the RevPAR decline was mostly in the top 25 U.S. hotel markets, but this time the gap between the top 25 (-3.5%) and all other U.S. hotel markets (-0.2%) was much larger and the largest of the past three weeks. Six of the top 25 markets saw double-digit RevPAR decreases led by Orange County (Anaheim) and including Atlanta, Houston, Las Vegas, San Diego and Washington, D.C.

Those six hotel markets saw sharp declines in RevPAR Sunday through Thursday. The weekend was better except in Houston, San Diego, and Washington, where the losses were similar. Weekday RevPAR for the top 25 in total was down 4.6% on falling occupancy. Houston and Las Vegas accounted for 150 basis points of the decrease. The former is due to difficult comps from last year’s late spring storms and the latter on the changing economic environment.

A fall in hotel group demand drove the weekday RevPAR declines in Atlanta, Las Vegas, and Orange County. Other top 25 markets seeing significant decreases in weekday group demand included Chicago, Nashville St. Louis, and Tampa Bay. Overall, weekly group demand across the U.S. – among all luxury and upper-upscale class hotels – was down 5%, which was the 10th consecutive decline. Group ADR, however, has continued to increase with the measure up 3.2%. Unlike total ADR, group room rates have been trending above the rate of inflation in nearly every week of the year.

New York City, Phoenix, Boston, Dallas, and San Francisco reported weekly RevPAR gains of more than 4% and all were mostly driven by rising ADR. New York also had the nation’s highest occupancy (88.2%) for the third consecutive week.

Events still matter

Outside the top 25 U.S. hotel markets, Columbia, South Carolina, had the nation’s largest weekly RevPAR increase (+44.2%) via an 83% weekend RevPAR gain. Other markets seeing weekly RevPAR growth greater than 20% included Louisville, Kentucky; Michigan South, Indiana North, Wisconsin North, West Virginia, and Mississippi. All, except Wisconsin North were driven by very large weekend RevPAR increases, which for the most part were due to college football games or special events such as the Bourbon and Beyond Music Festival in Louisville. Wisconsin North’s weekly RevPAR increase was due to a weekday gain.

For the ninth consecutive week, luxury led all hotel classes with RevPAR growth of 2.2%. In six of the past nine weeks, and for two consecutive weeks, it has been the only class with RevPAR growth. Economy was down 6.3% and has seen RevPAR decreases of 4.5% or more for 11 consecutive weeks. All other classes saw declines between 1.6% (upper upscale) and 3.4% (midscale) this week.

Global performance back on track

Excluding the U.S., global same-store hotel RevPAR bounced back the week of Sept. 7-13, up 6.8% on 4.5% ADR growth. A week ago, RevPAR growth had slowed by half. The difference this week was the return of occupancy gains as room rates continued to advance. Among the largest countries based on hotel supply, Italy, France, the U.K. and Japan all saw RevPAR increase by more than 11%, with Italy up 20.4%. On a non same-store basis (total), Italy was still strong with RevPAR up 13.3% and double-digit growth in luxury, upper-upscale and upscale classes. While nearly all Italian markets reported RevPAR increases and most seeing double-digit increases, Milan stood out with total RevPAR growth of 59.4% driven mostly by ADR.

For a third straight week, Mexico’s weekly RevPAR fell 6.4% with the Gulf of Mexico and Mexican Caribbean markets seeing the largest declines. On a same-store basis, the news wasn’t as bad. Both the aforementioned markets were still down, but Mexico as a whole was up 5% with only luxury-class hotels reporting a weekly decrease.

September not looking great

What should have been a positive week for the U.S. turned out to be even more negative than what was seen in the Labor Day week. Thus, our expectations for the week ending Sept. 20 are much more tempered. The following week has Rosh Hashanah, which will bring weekday travel to a standstill. Thus, don’t take the 1.3% month-to-date RevPAR growth to the bank just yet.

Keep in mind that a year ago September started on a Sunday while this year it began on a Monday. If you look at the data on a day-matched basis versus date-matched, you will find that U.S. hotel RevPAR is down 1.2% on falling demand (-0.4%). Occupancy is down 0.8% because of supply growth, while ADR is flat (+0.1%). For September RevPAR to be flat, in the 17 remaining days it has to increase by at least 0.7% every day, which could be a challenge. Since Aug. 1, the daily RevPAR average has been down 0.9%. Outside of the U.S., we expect little change in trend.

Isaac Collazo is senior director of analytics at STR.

This article represents an interpretation of data collected by CoStar's hospitality analytics firm, STR. Please feel free to contact an editor with any questions or concerns. For more analysis of STR data, visit the data insights blog on STR.com.