In the week of Aug. 17-23, U.S. hotel revenue per available room fell 1.3%, marking the third consecutive weekly decrease and 10th decline in the past 12 weeks.

Occupancy drove the retreat, but average daily rate also dipped 0.2%. Like in the past several weeks, the aggregate top 25 U.S. hotel markets were responsible for the RevPAR weakness (-3.8%). RevPAR in all other markets rose (+0.4%).

Industry decline influenced by two core markets

Hotels in Chicago and Houston accounted for most of the national RevPAR decline. If those markets were excluded, weekly RevPAR was flat nationally.

Compared with the week of last year’s Democratic National Convention, Chicago’s hotel RevPAR declined 19.9% on an ADR decrease of 22.3%. Even though ADR and RevPAR fell, Chicago’s hotel occupancy increased 2.2 percentage points. Further, Chicago’s hotel occupancy has increased in each of the last two weeks and in 26 of the past 34 weeks. The most recent gain was driven by seven of the eight Chicago submarkets. Chicago’s central business district, its largest submarket, saw occupancy advance 2.1 percentage points with occupancy of 76.9%. The Chicago central business district was also where the ADR impact from last year’s convention was most acute. Hotels in Chicago O’Hare Airport, Chicago Southwest, and Chicago South/Midway Airport also felt ADR and RevPAR declines.

Houston continues to face difficult comps from last year when late spring storms caused widespread flooding, resulting in increased room demand. In 2024, beginning in the week ending May 11 and through Aug. 31, Houston’s hotel demand rose by double-digits for 17 weeks except one. Thereafter, demand growth remained elevated. A year ago, Houston hotel demand was up 32%, while this year it’s down 29.5%. While all hotel classes are down in Houston, midscale and economy hotels are seeing the brunt of the decline as RevPAR is down by more than 50% in both those hotel types over the past four weeks and by the same amount in the most recent week. We expect the difficult comps to taper off over the next several weeks, but there will still be a drag on Houston’s hotel performance until the end of the year.

While Chicago and Houston were performance drags this week—as was Las Vegas in past weeks—the overall picture isn’t much rosier without them. U.S. hotel RevPAR over the past eight weeks has been flat to down and it doesn’t change much even when excluding economy-class hotels from all markets. This past week, 85 of the 172 STR-defined markets saw RevPAR decline, a number similar with what was seen in the fortnight, with 70 seeing a retreat in room demand.

Growth limited to the luxury class

Luxury hotels remained the only class growing RevPAR, which aligns with the past four weeks. The fall in upper upscale was centered on lower occupancy with most of the remaining classes driven by decreasing ADR—upper midscale’s decline was evenly split between the two. Note, the STR class structure includes independent (non-branded) hotels.

In the top 25 U.S. hotel markets, Houston and Las Vegas are driving a good amount of the RevPAR decline in hotels in the upscale and economy classes. Excluding those two markets, all classes, except luxury, are still down but to a lesser extent. Outside of the top 25 markets, RevPAR over the past four weeks was up in luxury, upper upscale and upscale with economy the only class seeing a significant decrease (-3.3%) on falling ADR.

Calendar changes in August and September to affect results

August will end with an extra Sunday this year, meaning that if nothing else changes, results for the month would still have been lower than a year ago. With the weakness seen so far – along with the extra Sunday – August will likely see a RevPAR decrease at or below what was seen in July even though the Labor Day holiday is expected to see record-breaking travel.

September will also be affected by the movement of Rosh Hashanah into the month from October a year ago. Essentially, September will only have two “clean” weeks for group and business travel.

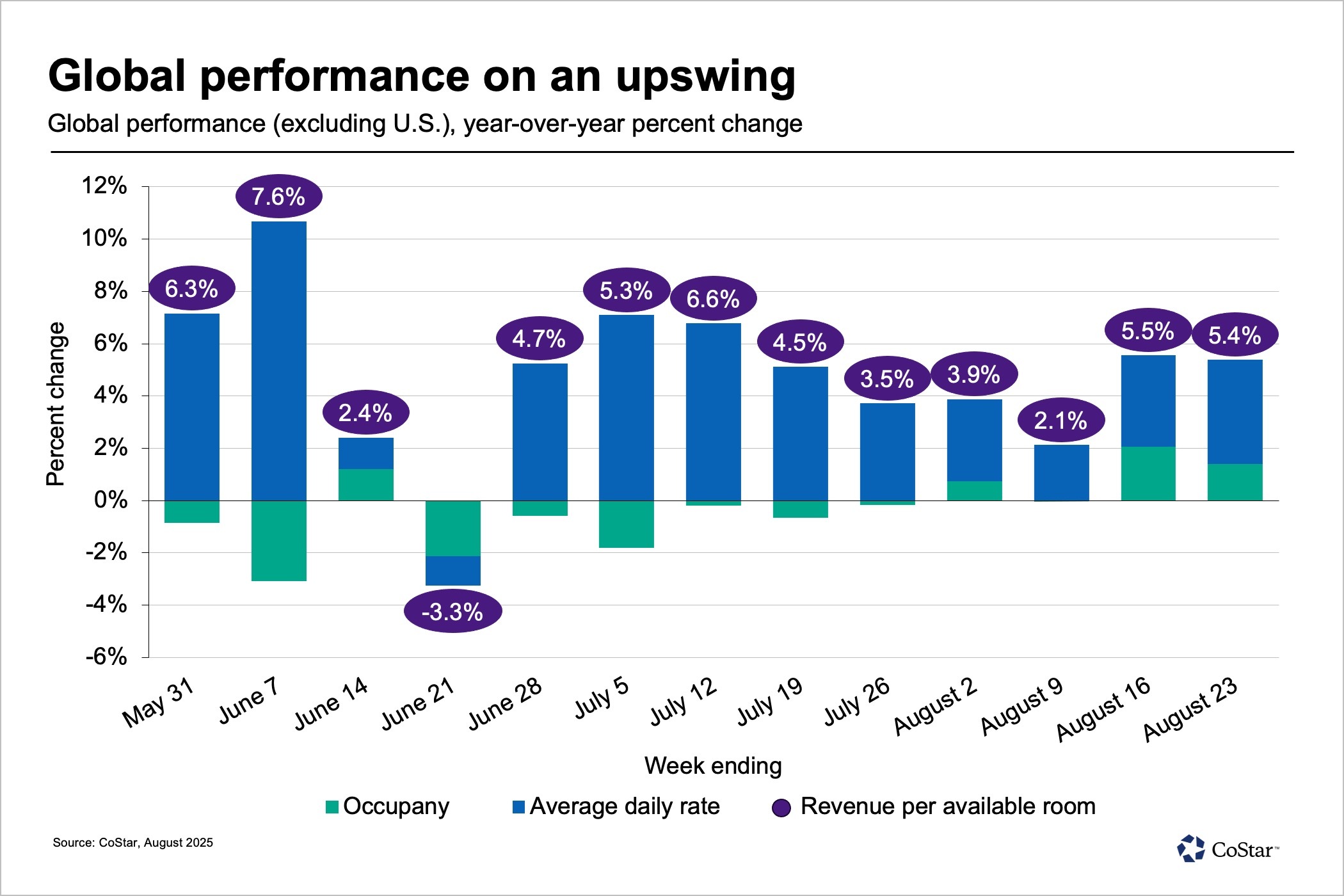

Hotels outside of the US see a fortnight of growth

Global hotel RevPAR — excluding the U.S. and based on comparable reporting hotels — increased 5.4% for a second consecutive week after four straight weeks of lower growth due in part to the Olympic comp in France. This week, France hotel RevPAR was up 24% after a 7% gain in the prior week and double-digit declines in three weeks before that.

Over the past four weeks, Spain, Italy, Canada, Japan, and United Kingdom posted hotel RevPAR increases of more than 5% with Spain in the lead. All of the five countries, except Italy, had hotel occupancy above 80%.

Canada’s hotel RevPAR has increased in 24 of the past 34 weeks, mostly on ADR. In the most recent week, RevPAR was up 4.9%. RevPAR has grown by more than 4% in May, June and July and is on track to see a similar gain in August.

Isaac Collazo is senior director of analytics at STR.

This article represents an interpretation of data collected by CoStar's hospitality analytics firm, STR. Please feel free to contact an editor with any questions or concerns. For more analysis of STR data, visit the data insights blog on STR.com.