NASHVILLE, Tennessee—When hoteliers show concern about supply, quite often their trepidation does not take into account hotel closures, which might mitigate some supply worries, sources say.

external

|

In the U.S., the last six years have shown a favorable relationship between supply and demand, said Lindsay Culbreath, senior director of marketing at STR, the parent company of Hotel News Now, although the number of rooms in the U.S. has increased by more than 60% in approximately the last 25 years.

Speaking at a Hotel Data Conference session tilted “Out with the old, in with the new,” Culbreath said in 1989 the U.S. had approximately 1.1 billion rooms, while today it has approximately 1.8 billion, according to STR data.*

Culbreath underlined the point that not every new hotel is automatically a +1.

To worry or not to worry? Here are five considerations on hotel closures, supply and demand to keep in mind:

1. Overall, fewer hotels are opening

Despite the current 1.8 million rooms in operation, the number of hotels opening in the U.S. is declining. In 2008, 1,400 hotels opened and in 2009, 1,382 opened, Culbreath said.

Yes, many of those 2008 and 2009 rooms were planned and in construction before anyone had heard of the last recession, but they opened in a period marked by diminished demand, she said.

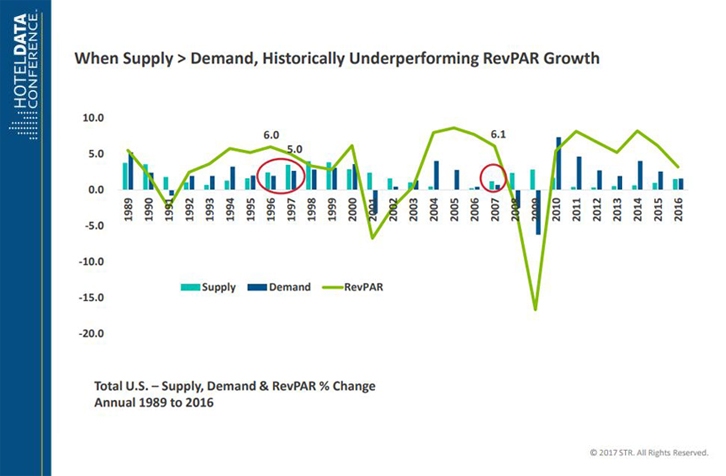

When supply is above demand, historically that results in poor revenue per available room, Culbreath added.

(Slide: STR)

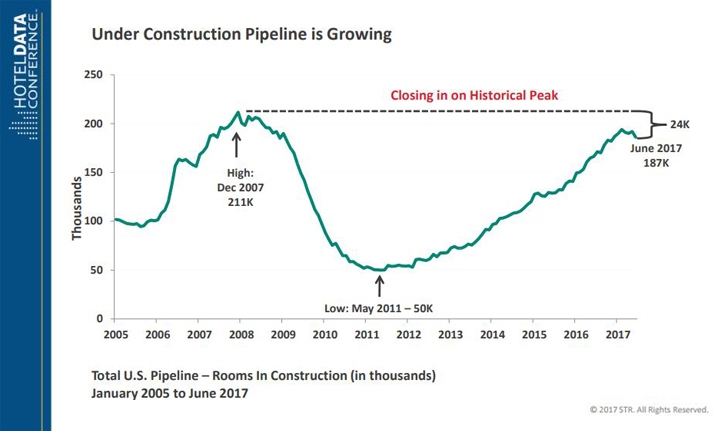

2. Supply is now close to 2007 numbers

Supply in rooms, if not hotels, today is roughly where it was in 2007, its historical peak, Culbreath said, but the difference today is that supply and demand are roughly at the same level.

Culbreath said the U.S. currently has 54,803 open hotels, with 156 under renovation, 4,806 under construction and 9,306 deemed permanently closed, demolished or adapted to another use.

The U.S. pipeline shows approximately 187,000 rooms in construction, with the historical peak being 211,000 keys in 2007.

“The turning point in development was 2012,” Culbreath said in regards to the steadily increasing numbers.

“We are seeing favorable supply and demand fundamentals over the past six years,” she said, reminding the audience that not all supply is bad.

(Slide: STR)

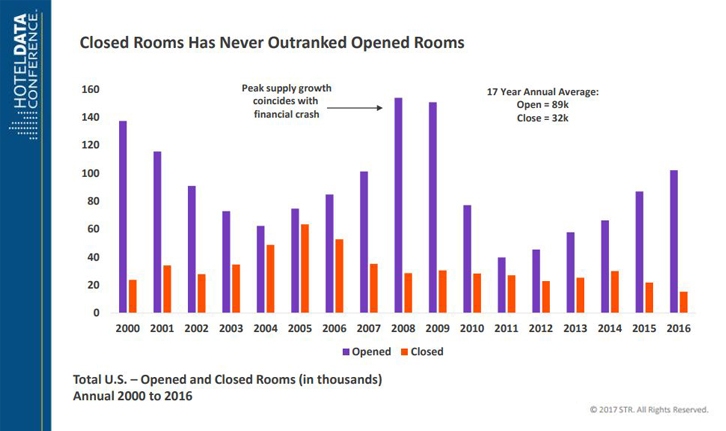

3. Fewer hotels are closing

Hotel closures are drastically declining.

“Closed rooms have never outpaced new rooms,” Culbreath said.

The increased demand for travel is what is keeping the industry buoyant, Culbreath said, as demand continues to outpace supply.

Added to the equation, Culbreath said, is the effect alternative accommodations have on hotel demand.

(Slide: STR)

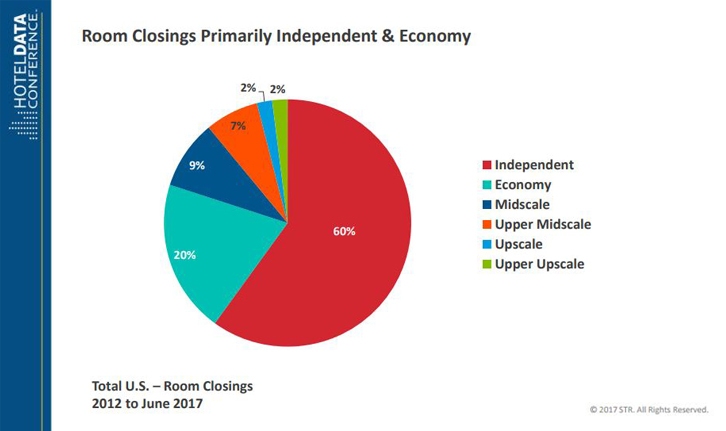

4. Of those closures, the majority are independents

Culbreath said that of those hotels that have closed since 2000, 60% of them have been independent properties.

Economy hotels constitute 20% of closures, while Upper and Upper Upscale assets constitute only 2% of closures during that period.

Unexpected events, notably those related to weather, also can change the picture although not all weather-related closures are permanent.

Culbreath cited Hurricane Katrina, which occurred in 2005 at a time when New Orleans had 1.2 million keys in 272 properties. Its devastation saw those numbers plummet to 360,000 rooms in 93 hotels. Today, it has 245 hotels, still well below its peak.

New Orleans’ RevPAR is at $101.81, close to its peak, helped perhaps by less supply.

Culbreath also mentioned Houston and its hotel performance data correlating to the decline in oil prices. (Her talk came before the storms and widespread flooding in the wake of Hurricane Harvey.)

(Slide: STR)

5. Select service enjoys lion’s share

Of the current 583,028 rooms under contract in June 2017, which is a year-over-year increase of 11.6%, most are in the upper midscale and upscale segments.

“Select service continues to dominate,” Culbreath said.

Economic events, though, have played havoc even on this segment in some markets, Culbreath said.

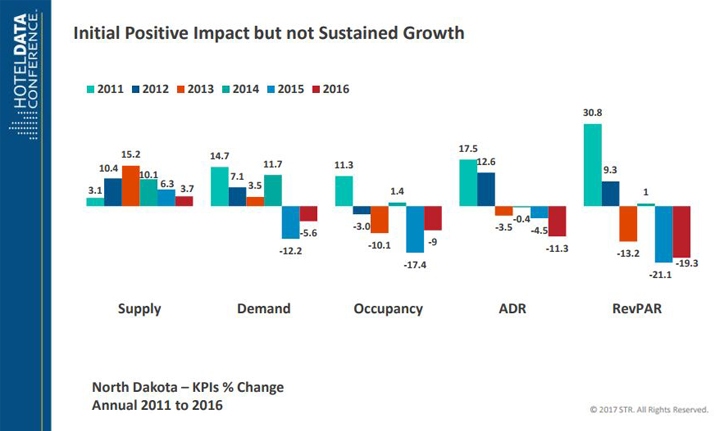

“North Dakota has never recovered from its new development boom,” Culbreath added, referring to that state’s recent uptick in shale gas extraction.

Culbreath said in January 2011, overall RevPAR in North Dakota was $53.47, rising to $76.84 in September 2012. In June 2017, that number went down to $42.22, approximately 21% down from January 2011 and approximately 45% down from September 2012.

(Slide: STR)

*Correction, 5 September 2017: An earlier version of this article reported the incorrect total number of rooms in the U.S.